Taking a Look at the Property Sector of Indonesia; Room for Recovery after the COVID-19 Crisis?

Just like most other sectors (with the notable exceptions of the digital economy and telecommunications sector) the property sector of Indonesia was heavily affected by the COVID-19 crisis in 2020-2021. Now this crisis has passed, it is interesting to take a look at the state of Indonesia’s property sector.

But first, let’s go back to Q3-2019 when no-one knew that a global crisis was about to emerge (out of the blue). Back then, Agung Wirajaya, Marketing Director at listed Indonesian property developer Agung Podomoro Land, said he saw clear signs that the property sector of Indonesia was about to experience a new boom that would peak around 2021-2022. He added that this would be part of the property sector’s cycle: every 10 years (or so) it experiences a peak in demand and supply.

The last time this peak occurred was in 2010-2013, when residential property prices in Indonesia rose by an average of 30 percent, per year. What explained this growth?

(1) Strong economic growth of Indonesia (with rapidly rising per capita GDP) amid the 2000s commodities boom (that officially ended in 2012); the rapidly expanding middle class meant that a growing number of Indonesians could buy property. It is interesting to point out that the majority of Indonesians can afford a house that has a price tag below IDR 500 million (approx. USD $33,000), which is a normal situation for a middle income country. For investors, this means their biggest market is among the lower middle class.

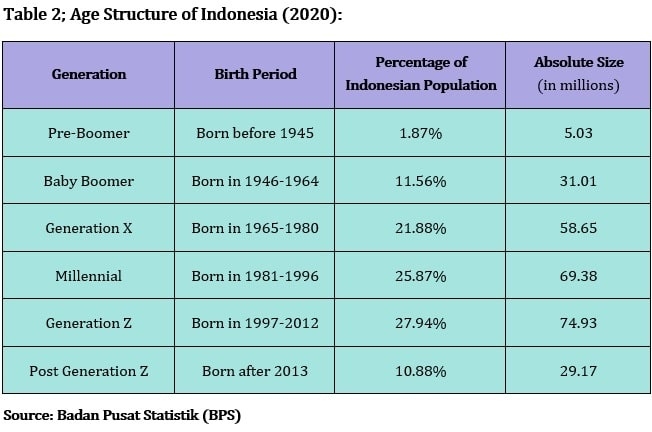

(2) Indonesia has a favorable demographic composition. Not only does it have a big population (around 275 million), but it also contains a young population as more than 50 percent of the population is below the age of 40 years. This implies that there will be many Indonesians seeking to buy their first home in the foreseeable future.

(3) In line with the global trend, Indonesia is experiencing a process of urbanization. Currently, more than half of the Indonesian population lives in urban areas and it is estimated that by 2050 two-thirds of the Indonesian population will live in the urban areas (based on a United Nations estimate). Amid such rapid urbanization, more and more houses, apartments and condominiums need to be built in Indonesia’s urban areas in order to meet future demand. Meanwhile, the limited availability of land in these urban centers gives rise to rapidly growing property prices (while developers need to focus on vertical property development – apartments and condominiums – in Indonesian cities to deal with the limited availability of land). Urbanization also means that there is a growing amount of property projects around the ‘traditional’ urban centers (referring to the development of suburbs where there still remains room for horizontal property development). And –albeit rare– we can also see the construction of brand new cities from scratch (an example being Indonesia’s capital city of Nusantara in East Kalimantan).

(4) For decades now, Indonesia has to cope with a massive housing backlog. Around ten years ago, this backlog was estimated at around 13.5 million houses. Today, the deficit is estimated at 12.7 million (which means that 12.7 million households are in need of a house). So, despite the Indonesian government’s ‘One Million Houses per Year’ program (which was launched in 2015, and targets low-income citizens) and despite private sector investment, the housing deficit remains wide. A crucial factor at play is that, each year, there emerge around 700,000 – 800,000 new households.

[...]

This is part of the introduction of the article (consisting of 34 pages; electronic report). To buy the article you can contact us by sending an email to [email protected] or a message to +62.882.9875.1125 (including WhatsApp).

Take a glance inside the report here!

Price of the article:

Rp 30,000