Latest Economic, Political and Social Updates from Indonesia

For Indonesia, the month of April 2021 was particularly dominated by the arrival of Ramadan, the holy fasting month for the Muslim community. From the evening of 12 April 2021 Muslims fast (typically from sunrise to sunset) up to 12 May 2021. It is also known as a period of intensified praying and reading the Qur’an for the Muslim community as well as higher focus on generosity.

Meanwhile, the Ramadan also has a significant impact on the economy of Indonesia. While on the one hand, economic activity generally tends to ease during this month as most people are not in the usual ‘work-mode’, it is spending on (and consumption of) food and beverage products that tends to peak in this period. Those who have ever visited a supermarket in Indonesia during Ramadan must have noticed that certain food and beverage products such as biscuits, dates, and syrup are suddenly piled up in the middle of stores (often available at discounted prices). The reason is clear. Demand for these items rises amid Ramadan (as these products are consumed and shared among family or friends when breaking the fast in the late-afternoon or early evening, or, given as presents when visiting family or friends).

And, it is not only snacks or syrup that are in high demand. Typically, demand for a range of food items rises during Ramadan (such as chicken meat, eggs, beef, garlic, and red chili pepper), especially when approaching Idul Fitri or Lebaran (referring to the festivities that mark the end of the Ramadan), as people take more effort to organize ‘dinner parties’ in the evening (or cook food at home and then give part of it to their neighbors; a sign of generosity).

What this means is that, normally, inflation tends to peak in Indonesia in this period (moreover, particularly prior to the Joko Widodo administration, inflationary peaks were particularly high around Ramadan because the central government was often late in allowing more imports of certain food items when domestic supplies became scarce, such as garlic, while there were also ‘naughty’ importers or stakeholders – for example the ‘beef mafia’ – who deliberately waited for stocks to become scarce on the market, hence causing prices to rise, before delivering new supplies).

However, the difference this year (and last year) is that we are still in the middle of the COVID-19 crisis. So, we should not expect to see normal rates of consumption yet. In many urban areas on Java, Sumatra and Bali there are still social and business restrictions that aim at limiting people’s gatherings, while part of the population has seen its spending power being reduced in the crisis (for example because they were laid off or saw a wage cut). Others may simply be too concerned to go out and meet other people amid the pandemic.

The tables below show how the COVID-19 crisis managed to drag down household consumption in Indonesia since Q1-2020 (and considering household consumption accounts for around 57 percent of total economic growth, it significantly ‘helped’ to push the Indonesian economy into a recession).

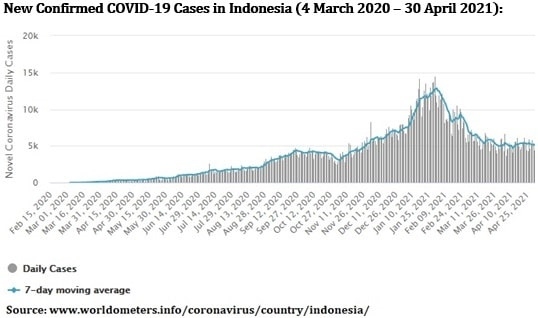

So, consumption across Indonesian society should remain under par in this year’s Ramadan and Idul Fitri (compared to Ramadans and Idul Fitris in the pre-COVID-19-crisis era). However, compared to preceding months (well, the past 12 months actually) we should see a clear improvement in consumption, partly thanks to the special ‘holiday bonuses’ that are sent to workers and staff in the formal sector, but also because restrictions are currently less tight than during last year’s Ramadan, while people may also be less concerned as the COVID-19 virus turned out to be less fatal than initially reported by the World Health Organization (WHO) in early 2020. Moreover, the number of new confirmed COVID-19 cases has dropped significantly over the past couple of months. So, this should make people more willing to spend.

Nonetheless, the mudik (referring to the exodus of millions of city-dwellers to their places of origin -usually in the suburban or rural regions- where they typically spend a few days to celebrate Idul Fitri) was banned by the Indonesian government for the second year in a row. This too has economic implications as the mudik tends to give rise to a significant money rotation in the country, where money flows from urban to regional areas. This topic is discussed in more detail in one of the chapters in this report.

Still, besides the Islamic celebrations (and mudik ban as well as related restrictions), the month of April 2021 was a relatively quiet month for Indonesia. Pressures on the country’s economy and financial conditions seem easing (reflected by a benchmark stock index and rupiah rate that are moving sideways, which is a pleasant change from the weakening trends we detected in the preceding month), while the number of new confirmed COVID-19 cases in Indonesia remains under control.

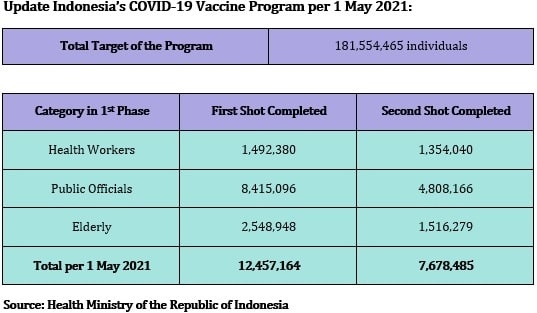

However, while the context seems to improve, we still stand by our earlier estimate that Indonesia’s GDP will contract by 0.5 percent year-on-year (y/y) in Q1-2021, hence extending the economic recession (but this recession should end in Q2-2021, especially thanks to the low base effect), while we also feel that the impact of the COVID-19 pandemic (on the Indonesian economy) will probably continue to be felt for an extensive period of time, possibly even extending into 2023 as we expect the existing COVID-19 immunization programs to be partly ineffective. For example, the efficacy rate of Sinovac could be as low as 50 percent, while we also fear that certain COVID-19 mutations may not be curtailed by the existing vaccines. Moreover, if the government fully depends on vaccines to combat the virus and will only fully open the economy once the immunization program has been completed, we may need to wait a long time. Per 1 May 2021, a total of 7.68 million Indonesians had received their second (and final) shot in the immunization program, according to Indonesia’s Health Ministry. Considering the central government aims to vaccinate 181.5 million people to reach herd immunity, and considering Indonesia’s immunization program started in mid-January 2021, it could take years before the program is completed.

Regarding events in April 2021, two more notes. First, there was a cabinet reshuffle that was orchestrated by President Joko Widodo at the end of April 2021 (which had been approved by the House of Representatives, DPR, on 9 April 2021). However, it was a minor reshuffle only, albeit a quite unusual one as it merged the Ministry of Education and Culture with the Ministry of Research and Technology to create the Ministry of Education, Culture, Research, and Technology (headed by Nadiem Anwar Makarim who previously served as Minister of Education and Culture). The reshuffle also introduced the Ministry of Investment (headed by Bahlil Lahadalia who served as Chairman of the Indonesia Investment Coordinating Board, BKPM, so the BKPM has simply been turned into a ministry). Lastly, Laksana Tri Handoko was appointed as Head of the National Research and Innovation Agency (or BRIN), which has now become an independent state body.

Do we expect this reshuffle to make a significant impact? Well, not really, although in terms of Indonesia’s investment environment there is the interesting difference that – previously – the BKPM was only able to execute laws and regulations made by the government or ministries (as it was a non-ministerial agency). However, now the BKPM is turned into a ministry it has the power to make and impose regulations by itself.

This could help to smoothen the investment environment because at the BKPM they should know what and how the flow of investment is disrupted into the country. So, this should put them in a position where they can formulate regulations that help to ease these obstacles. However, considering Indonesia is plagued by thick layers of red tape and there are other structural bottlenecks too (that are beyond the scope of the Investment Ministry), we certainly do not expect to see any sudden and major changes as a consequence of the reshuffle.

Secondly, in April 2021, there was also a national tragedy that became a big topic in the local news (a story that was also picked up by the international press), namely the sinking of Indonesian navy submarine KRI Nanggala 402, with a crew consisting of 53 men. Contact was lost with the submarine in the early morning of 21 April 2021 after it was given permission to dive for a torpedo firing exercise.

Several hours later an oil slick was spotted in the area as well as the smell of diesel fuel. From around the world, navy ships joined the search mission over the next few days. Considering the submarine would be without oxygen within a few days, hurry was needed. However, objects from the missing submarine started to be found floating in the Bali Sea. Later, an underwater scan confirmed the submarine had sunk to a depth of 838 meters below the surface of the sea and had split into at least three parts, implying that there was no hope any of the 53 crew had survived the disaster.

Experts suspect it was either a very strong internal solitary wave, which is known to occur in the seas around Bali, that pushed the submarine vertically toward the ocean floor, or, material or mechanical failure that caused the catastrophic flooding of one or more compartments inside the submarine (the KRI Nanggala 402 was old as it was built in 1978 and last overhauled in 2012, so metal fatigue could be at play).

What makes the disaster even more sensitive (especially for the families of the crew) is that it might be impossible to bring the diseased back to the surface. It is not only the sheer depth at which the submarine is positioned that makes it problematic to bring their remains onshore but it’s also the fact that the submarine carried torpedos that may have been damaged at impact on the ocean floor. This makes it very risky for rescue teams to do their job.

Lastly, we want to thank you for purchasing this April 2021 edition of our monthly report, and we hope it contains valuable or interesting information for you!

CV Indonesia Investments

Yogyakarta, Indonesia

2 May 2021

The April 2021 report can be ordered by sending an email to [email protected] or a message to +62.882.9875.1125 (including WhatsApp).

Price of this (electronic) report:

Rp 150,000

USD $10,-

EUR €10,-

Take a glance inside the report here!

.