Gross Domestic Product of Indonesia

Between the years 1965 and 1997 the Indonesian economy grew at an average annual rate of almost seven percent. This achievement enabled Indonesia to graduate from the ranks of 'low income countries' into that of the 'lower-middle income countries'. However, the Asian Financial Crisis that erupted in the late 1990s had a dramatic impact on the Indonesian economy, prompting a contraction in gross domestic product (GDP) of 13.6 percent in 1998 and limited GDP growth of 0.3 percent in 1999. This crisis rocked the economic and political foundations of Indonesia, and would usher in the start of a new era with new challenges and opportunities.

The Asian Financial Crisis allowed a re-start for Indonesia by building governance with a focus on prudent fiscal policies and with authorities (such as Bank Indonesia, and later joined by the Financial Services Authority/OJK) that could actually monitor the money flows within the country (including the private sector's foreign debt). Partly thanks to prudent fiscal policies, Indonesia was not badly affected by the global financial crisis in 2007-2008. It, in fact, weathered the storm quite comfortably (below we discuss this in more detail).

However, in 2020, another major crisis broke out: the novel coronavirus (COVID-19) crisis. This one was a truly unprecedented crisis as no-one saw it coming and it affected the entire world, causing the complete collapse of consumption (including tourism), production, investment, and trade. Indonesia, which had just graduated from 'lower-middle income country' to 'upper-middle income country' with gross national income (GNI) per capita at USD $4,050 in 2019, fell back into the category of 'lower-middle income countries' due to four straight quarters of negative economic growth between Q2-2020 and Q1-2021.

Summary and Focus of this Analysis

In the aftermath of the Asian Financial Crisis, roughly between the years 2000 and 2004, Indonesia experienced a period of economic recovery with an average GDP growth of 4.6 percent per year. Hereafter, Indonesia's GDP growth accelerated, with the exception of 2009 when, amid global financial turmoil, uncertainty and massive capital outflows, Indonesia's GDP growth fell to (a still admirable) 4.6 percent. This period of recovery and impressive accelerating economic growth between 2000 and 2011 can particularly be attributed to two (inter-related) matters:

(1) Growing household consumption (amid rapidly strengthening per capita GDP and purchasing power), which caused household consumption to become the cornerstone of the Indonesian economy; and

(2) the 2000s commodities boom.

In fact, there is a very strong correlation between swings in commodity prices and trends in Indonesia's household consumption: when commodity prices are high, consumption rises. However, when commodity prices are structurally declining for a prolonged period, then Indonesia's household consumption experiences hiccups. And considering household consumption now typically accounts for about 56-58 percent of Indonesia's total economic growth, it therefore has a direct and significant impact on the country's GDP.

Indonesia’s GDP Growth Rate 1961-2019:

What is interesting about the graph above is that Indonesia’s GDP growth shows high volatility between 1960 and 1990, but a much more consistent GDP growth level after 1990 (with the notable exception of the Asian Financial Crisis in the 1997-1999 period). What is visible here is that the emergence of the middle class (becoming a huge consumer force) made Indonesia's GDP growth much more consistent or stable after 1990, and making Indonesia less dependent on volatile commodity price swings on international markets. However, despite becoming less volatile on a year-on-year basis, commodity prices do still influence the longer term trends of Indonesia's GDP, hence we see a rising trend between 2000-2011 (when the impact of the '2000s commodities boom' lifted the Indonesian economy) but deceleration, followed by modest acceleration and stagnation, in the 2011-2020 period (when commodity prices cooled). Starting from the second half of 2020 commodity prices are back up - particularly thanks to China's recovery from the COVID-19 crisis - causing some analysts to claim that we are at the beginning of the 2020s commodities supercycle. Whether structural or not, high commodity prices since the second half of 2020 certainly help Indonesia to exit the COVID-19 crisis.

But besides allowing the acceleration of Indonesia's economic recovery after the Asian Financial Crisis, the 2000s commodities boom can now also be seen as a time of missed opportunities as the Indonesian government failed to reduce the country's traditional dependency on (exports of raw) commodities. Hence, when commodity prices collapsed after 2011 Indonesia's economic expansion started to slow accordingly. Between 2011 and 2015 a period of worrying economic slowdown emerged, with GDP growth dipping below 5 percent year-on-year (y/y) in 2015. So, in case commodity prices will again experience a supercycle in the 2020s, the Indonesian government should not reduce its focus on encouraging the development of value-added activities this time, while encouraging the integration of Indonesia into the world's (value-added) supply chains (which has remained relatively weak so far). Further improving the investment environment is also crucial as it will attract foreign direct investment that brings valuable new technology and expertise to Indonesia (and tends to integrate Indonesia into the global supply chains in case of export-oriented investment).

Under normal circumstances, the Indonesian economy expands at a pace of around 5 percent (y/y) particularly thanks to household consumption. While most countries envy that growth pace, the concern in the case of Indonesia is that growth around 5 percent fails to generate enough job opportunities for the country's huge labor force. Moreover, Indonesia will encounter difficulty avoiding the 'middle-income trap' if it fails to secure accelerated economic growth above 5 percent (y/y), structurally.

In this article we discuss the recent economic performance of Indonesia, Southeast Asia's largest economy, starting from the end of the 2000s commodities boom. We divide the subtopics in the following categories:

- The economic slowdown that occurred after the end of the 2000s commodities boom in the 2010-2015 period;

- The period of slowly accelerating economic growth that occurred between 2015 and 2019, and;

- The sudden economic collapse amid the global COVID-19 crisis.

For an analysis of Indonesia's economic growth during the New Order government, or an analysis of the causes and consequences of the Asian Financial Crisis, click on one of the links in the text.

Chapters in Indonesia's Recent Economic History:

| Years | Average Annual GDP Growth (%) | Period |

| 1967 – 1997 | 6.85 | Suharto's New Order |

| 1998 – 1999 | -6.65 | Asian Financial Crisis |

| 2000 – 2004 | 4.60 | Recovery |

| 2005 – 2011 | 5.80 | 2000s Commodities Boom |

| 2011 – 2015 | 5.53 | Slowing Economic Growth |

| 2015 – 2019 | 5.03 | Slowly Accelerating Economic Growth |

| 2020 – 2021 | COVID-19 Crisis |

Gross Domestic Product (GDP) Statistics Indonesia:

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

| Nominal GDP (in billion USD) |

890.8 | 860.9 | 931.9 | 1,015.0 | 1,042.2 | 1,119.2 | |

| GDP (annual % change) |

5.01 | 4.88 | 5.03 | 5.07 | 5.17 | 5.02 | -2.07 |

| GDP per Capita (in USD) |

3,492 | 3,332 | 3,563 | 3,838 | 3,894 | 4,135 | 3,912 |

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |

| Nominal GDP (in billion USD) |

432.2 | 510.2 | 539.6 | 755.1 | 893.0 | 917.9 | 912.5 |

| GDP (annual % change) |

6.35 | 6.01 | 4.63 | 6.22 | 6.17 | 6.03 | 5.56 |

| GDP per Capita (in USD) |

1,861 | 2,168 | 2,261 | 3,122 | 3,643 | 3,694 | 3,624 |

The base year for computing the economic growth rate shifted from 2000 to 2010 in 2014, previous years have been recalculated

Source: World Bank

When taking a look at the tables above one may notice that the global economic downturn brought about by the global financial crisis in the late 2000s had a relatively small impact on the Indonesian economy (compared to the impact it had on other countries). In 2009, Indonesia's GDP growth dropped to +4.6 percent (y/y), which meant that the country was actually among the top GDP growth performers worldwide that year (and the third-highest among the G20 group of major economies).

So, despite severe global turmoil (which led to a big decline in global trade and investment), the economy of Indonesia was still able to grow at an admirable pace in 2009. What was the key to this success?

Well, firstly, one very crucial matter is that Indonesia is not only home to a huge population (the fourth-largest worldwide) but also home to a population that saw its per capita GDP and purchasing power rise sharply throughout the 2000s on the back of the commodities boom and overall economic growth. As a consequence, household consumption now contributes significantly (some 56-58 percent) to the country's total economic growth (a side-effect of high commodity prices was that investment soared). The 2000s commodities boom greatly helped to turn the Indonesian population into an impressive consumer force (particularly thanks to the country's rapidly expanding middle class). Household consumption was a 'cushion' for the Indonesian economy that allowed sustained economic activity at a time when the global economy and global conditions turned sour.

Secondly - and this is a structural weakness of the Indonesian economy - its export and import performance forms only a relatively small percentage of the country's total economy. Indonesia's trade-to-GDP ratio is in fact very low at around 40 percent (far below the world's average of 55-60 percent). This low ratio indicates that Indonesia is poorly integrated into the global supply and value chains. It is a situation that implies missed opportunities in terms of foreign investment (missing out on new technology and expertise that foreign investments tend to bring), new employment opportunities, and - more generally - missed opportunities in terms of economic and social growth.

The only 'advantage' of having a low trade-to-GDP ratio is that the country is not heavily affected by a sudden drop in international trade as happened in 2008-2009 (global financial crisis) and in 2018-2020 (in the context of - first - the United States-China tariff war and - second - the COVID-19 crisis). However, it means that in good trade times, Indonesia is left behind (mainly relying on unprocessed commodities).

So, Indonesia's huge domestic market (Indonesia being home to around 270 million people) and its relative 'immunity' to sudden drops in global trade (as well as drops in foreign investment inflows as foreign investment as a percentage of GDP is also typically weak for Indonesia), means that Indonesia will not see huge contractions in times of global crises. For comparison, Singapore (which is highly dependent on international trade and investment) experienced a 5.8 percent (y/y) economic contraction in 2020 amid the COVID-19 crisis. Indonesia managed to keep the damage at 2.07 percent y/y in that same year).

Indonesia's Middle Class - Engine of Economic Growth

In 2010 the World Bank noted in a report that, amid robust economic growth, around seven million Indonesians were added to the country's middle class, each year. And while the inflow into the country's middle class has been curtailed as economic growth has slowed down, Indonesia still contains a massive consumer force that drives the economy and triggers rising domestic and foreign investment, today. Obviously, investors are eager to invest in a country that has a population of 270 million people (with rising per capita GDP) as it means there exists a huge market for a whole range of products and services, especially on densely-populated Java.

Determining the exact number of middle class Indonesians is a matter of definition. At the start of 2020, the World Bank mentioned that around 52 million Indonesians fall within its middle class category (which roughly equals 20 percent of the total population of Indonesia).

However, other research companies, such as the Boston Consulting Group (BCG), McKinsey, and Oxford Business Group, set a lower bar and thus their number of middle class Indonesians is about two times higher. But all agree that Indonesia's middle class will continue to grow rapidly. And this rapidly increasing number of middle income earners is a huge potential for further (structural) economic growth in the years - and decades - to come.

Already, the Indonesian middle class has been a major driver of economic growth as this group’s consumption has grown about 12 percent, annually, since 2002 and now represents close to half of all household consumption in Indonesia.

Slowing Economic Growth (2011-2015)

While Indonesia experienced strong economic growth in the years 2010-2012 (with slightly over 6 percent in each of the three years) in the aftermath of the global financial crisis in the late 2000s, it was also the start of Indonesia's economic slowdown. Beginning from 2010, Indonesia's annual GDP growth started to ease, and there are several factors that explain this slowdown:

• Sluggish Global Economic Growth; China in Focus

After a strong rebound in 2010 (from the global recession that was felt around 2007-2009), the pace of global economic growth slowed and stabilized around a lackluster 3.5 percent (y/y) between 2012 and 2016.

It was particularly the rapidly moderating economy of China that caused concern about global growth. China, which overtook Japan as the world's second-largest economy in 2010, had been a major engine of economic growth in the 2000s and early 2010s (with annual GDP growth figures of +10 percent). However, in 2010 China began to shift its economic growth model (which previously relied on investment and exports) to an economic model that depends on private consumption, services and innovation. This shift is a process that requires time and effort.

The reason for this shift was that such reforms are required so that China can escape the middle-income trap (this is a trap that can occur when a country reaches a certain economic level but begins to experience a sharp decline in the rate of economic growth because it cannot adopt new sources of economic growth, such as innovation).

Meanwhile, a rapidly aging population, a declining birth rate, a US Federal Reserve that was increasingly tightening monetary policy between 2013-2019, and the slowing global economy also put the brakes on the Chinese economy. In addition, China's economy was also affected by tough regulations on debt and certain types of risky loans, which then triggered a sharp slowdown in investment in China. Lastly, China's decision to make its economy more dependent on the domestic market could also be related to troubled international relations in the 2010s.

As a result, the rate of growth of the Chinese economy dropped dramatically, and has dragged down world economic growth. In 2019, the Chinese economy grew at a rate of 6.1 percent (y/y), the lowest level in 30 years (but a level that may need to be considered the 'new normal' for China). Indeed, China's economic growth rate fell much further in 2020 (to 2.3 percent y/y), but this was the consequence of the heavy COVID-19 crisis.

GDP Growth of China:

| (2005) | (2010) | 2016 | 2017 | 2018 | 2019 | 2020 | |

| GDP (annual % change) |

(11.4) | (10.6) | 6.8 | 6.9 | 6.7 | 6.1 | 2.3 |

Source: Macrotrends.net

The slowing down of economic expansion in China has a direct impact on Indonesia because the two countries are important trading partners (China accounts for almost one tenth of Indonesia's total exports). It is estimated that for every 1 percent decline in Chinese GDP growth, Indonesia's economic expansion decreases by 0.3 percent. So, the structural decline in China's economic growth certainly contributed to the structural decline in Indonesia's economic growth in the first half of the 2010s.

Related to the paragraph above, with China being the second largest economy in the world (after the United States) and a huge importer of commodities, weak economic growth in China caused a sharp decline in demand for commodities in the 2010s, and thus a fall in commodity prices.

• Sliding Commodity Prices

The commodities boom in the 2000s, when commodity prices increased rapidly (due to sharply rising demand in several emerging markets, especially China), was a very lucrative period for Indonesia because the country holds large reserves of crude palm oil (CPO), coal, gas, and copper. The 2000s commodity boom also managed to accelerate Indonesia's recovery from the Asian Financial Crisis.

However, the global economic slowdown in the 2011-2015 period (and especially the slowdown of the Chinese economy) resulted in commodity prices falling to very low levels. The chart below shows the sharp decline in commodity prices between the beginning of 2011 and the end of 2015.

Commodities Index:

Being a large commodity exporter (and lacking well developed downstream industries, while its commodities are often exported in raw form), Indonesia's export performance is heavily affected when commodity prices (such as coal and crude palm oil) are low. This then also impacts negatively on Indonesia's overall economic growth.

It is also interesting to add here that the low commodity prices after 2011 are not only caused by subdued global demand but also because of excess supply. During the 2000s commodity boom era - and also after the end of the great global recession in the late 2000s - institutions such as the World Bank and International Monetary Fund (IMF) released global growth projections that were far too optimistic, and thus many companies decided to enter the commodity sector, while established commodity companies invested in the expansion of production capacity, resulting in a supply glut that pushed down commodity prices in the first half of the 2010s.

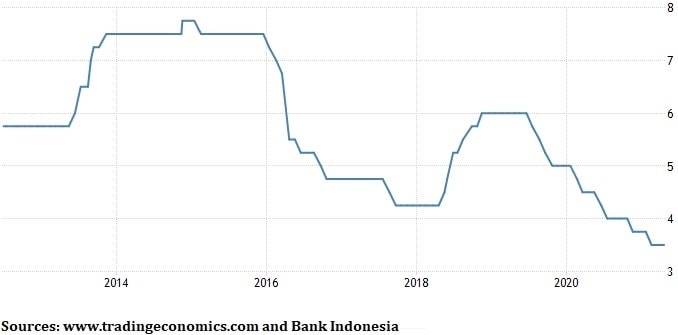

• Bank Indonesia's High Interest Rate Environment:

High interest rates curb credit growth, and thus curb economic growth. Starting from mid-2013, the central bank of Indonesia (Bank Indonesia) raised its benchmark interest rate (back then the 'BI rate' was still in use) gradually, yet aggressively, from a low of 5.75 percent to 7.75 percent at the end of 2014. Bank Indonesia decided to tighten its monetary policy in order to combat high inflation (which had risen sharply after several fuel subsidy reforms), ease pressures on the country's wide current account deficit, and support the rupiah rate that had become burdened by heavy pressures from mid-2013 due to monetary tightening in the United States (known as the 'taper tantrum', referring to the 2013 collective reactionary panic that triggered a spike in US treasury yields after investors learned that the Federal Reserve was slowly putting the breaks on its quantitative easing program).

Massive capital outflows from developing countries, including Indonesia, occurred for most of 2013 as the US Federal Reserve hinted at winding down its USD $85 billion monthly bond purchasing program (US quantitative easing). In 2015 these capital outflows from developing countries reappeared because the world started to prepare for higher US interest rates (Fed Funds Rate). In December 2015 the Federal Reserve would raise its key rate for the first time in almost a decade, from the range of 0.0 - 0.25 percent to 0.25 - 0.50 percent.

Indonesia's Benchmark Interest Rate:

• Indonesian Politics:

2014 was a big 'political year' for Indonesia because of the legislative and presidential elections. The presidential election was a battle between Joko Widodo, supported by the PDI-P party, who was also the market-favorite due to the reform-minded nature he showed as mayor of Solo and governor of Jakarta. His opponent was Prabowo Subianto, supported by Gerindra. Subianto is a controversial former army general who was also former President Suharto's son-in-law. Although at first this 2014 election was believed to become an easy victory for Widodo, the presidential election in fact turned out to be a fierce and narrow battle (that would eventually even require a decision by the Constitutional Court to confirm the outcome). As a consequence of the high degree of political uncertainty in the context of the 2014 elections (after the decade-long Susilo Bambang Yudhoyono period), investment was disrupted for about five months in 2014, contributing to the further slowdown of the Indonesian economy.

Because Indonesia is a young democracy, contains a very diverse society, and has many swing voters (i.e. people who are not loyal to one political party), there is always a chance to see a big surprise in elections. Therefore, elections in Indonesia always give rise to a high level of uncertainty. And, if there is one thing investors hate, it is uncertainty.

Regulatory and legal uncertainty regarding the government's (economic) policies has been one of the main obstacles in Indonesia's investment environment because it makes investors think twice before deciding to invest in Indonesia (see also the Risk section). For example, in line with the 2009 Mining Law, Indonesia suddenly imposed a ban on the export of mineral ores in January 2014. And while this ban was not immediately implemented in full (as miners could continue exporting mineral seeds if they committed to establishing domestic smelter facilities and paying higher taxes and royalties), and while the objectives of the new policy are good (namely reducing Indonesia's dependence on highly volatile commodity prices), the new law was an example of how uncertain business in Indonesia is (due to sudden changes in regulations). It was actually a violation of miners' contacts.

Another political matter that generally undermines Indonesia's economic expansion is slow and ineffective government spending. Because of red tape (excessive bureaucracy), corruption, and weak coordination and cooperation between government institutions (both at the central and regional levels), government spending is not optimal.

• Stagnating Household Consumption Growth:

Meanwhile, household consumption growth stagnated in Indonesia (see table below) after having accelerated rapidly in the 2000s. Considering household consumption contributes around 56-58 percent to Indonesia's total economic growth, stagnating household consumption growth has a significant and immediate impact on the country's macroeconomic growth: household consumption growth around 5.0 percent (y/y) makes it very hard for Indonesia's overall economic growth to accelerate.

The reason behind stagnant household consumption growth remains somewhat of a mystery and has been confusing analysts and policymakers. However, given that third-party funds in Indonesia's banking sector have grown over the same period, it could indicate that consumer purchasing power did actually not weaken. Instead, Indonesian consumers could be saving their money (on bank accounts), rather than spending it. Some argue that this shows a structural change: the younger generations (millennials) are more aware of the importance of depositing funds in bank accounts, while the older generations of Indonesians lack such awareness. And over time, the role of the younger generations has increased in the Indonesian economy, implying that changes in spending behavior were increasingly felt in the economy.

However, we also want to remind that the end of the 2000s commodities boom in 2011 has undermined Indonesia's per capita GDP growth, implying that household consumption growth could not continue at the same pace.

Growth of Indonesia's Household Consumption in 2010-2015:

| 2010 | 2011 | 2012 | 2013 |

2014 | 2015 | |

| Growth (annual % change) |

5.00 | 4.70 | 5.28 | 5.43 | 5.16 | 4.96 |

Source: Badan Pusat Statistik (BPS)

Period of Slowly Accelerating Economic Growth (2015-2019)

The Indonesian economy continued to experience the negative impact of slowing economic growth in China and sluggish global economic growth in the period 2015-2019. And, as a consequence of sluggish growth across the world (and particularly in China) commodity prices continued to show a downward trend. This was a very difficult context for the Joko Widodo administration, which had been inaugurated in late-2014, to achieve strongly accelerating economic growth. And, unfortunately, many Indonesians had high hopes for rapid growth, especially since President Widodo had pledged (during his presidential campaign) to bring Indonesia back to an annual economic growth rate of 7 percent (y/y). With a proven track-record as mayor of Surakarta (Central Java) and governor of Jakarta, Widodo was regarded a reform-minded leader, hence the favorite of investors. Moreover, he does not originate from the country's traditional political or military elite. This elite, which had been formed in the New Order, is steeped in corrupt practices, while political policies were often made with specific business interests in mind.

Shortly after taking office, Widodo made a very important decision - one that was applauded by many analysts - namely: slashing the government's energy subsidy spending (mainly fuel and electricity). The table below shows a huge cut in subsidy spending starting in 2015 (compared to 2014, the last year of the second Susilo Bambang Yudhoyono administration). The trillions of rupiah that had been cut in the subsidy bill were redirected to infrastructure development spending and social spending. All analysts were very pleased seeing this decision as many had criticized Indonesia's ballooning energy subsidy spending because it was considered misdirected (failing to support the poor) and prevented heavy government spending on productive matters (such as social development and infrastructure). This decision also helped Indonesia to obtain investment grade ratings from the big three credit rating agencies (Standard & Poor's, Moody's Investors Service, and Fitch Group), thereby unlocking a new pool of capital inflows.

The structural lack in quality and quantity of infrastructure development in Indonesia started to really show in the 2000s. Since the end of Suharto's authoritarian New Order regime there had been under-investment in the country’s infrastructure, resulting in high logistics costs (making Indonesian businesses less competitive compared to foreign counterparts), and making investors think twice before investing in the country. The lack of infrastructure development involves both hard infrastructure (such as roads, harbors, and electricity) and soft infrastructure (such as healthcare and law enforcement). Meanwhile, successful infrastructure projects should have a multiplier effect on the Indonesian economy as it tends to attract private investment.

However, the table also shows that in 2018 and 2019 the government became more generous again. This is most likely related to the legislative and presidential elections of 2019 (administrations typically become very generous ahead of national elections as it boosts their chances in the race). And, indeed, for the 2020 budget - after the elections - the government had again cut energy subsidy spending significantly.

Indonesian Government's Subsidy Spending:

| 2013 | 2014 | 2015 | 2016 |

2017 | 2018 | 2019 | 2020 | |

| Subsidy Spending (IDR trillion) |

355 | 392 | 186 | 174 | 166 | 217 | 224 | 187 |

| - Energy | 310 | 342 | 119 | 107 | 97 | 154 | 160 | 125 |

| - Non-Energy | 45 | 50 | 67 | 67 | 69 | 63 | 64 | 62 |

Source: Finance Ministry of Indonesia

Widodo also immediately started to focus on improving the investment environment of Indonesia in a bid to attract more private investment. One of the biggest obstacles to investment in Indonesia is the high degree of bureaucracy. The country’s bureaucracy had become a 'power centre' in its own right. In an effort to simplify the licensing system for investment projects, Indonesia launched its integrated one-stop service center (Pelayanan Terpadu Satu Pintu, abbreviated PTSP) at the Indonesia Investment Coordinating Board (BKPM) in late January 2015. However, the PTSP only very modestly improved the country's tough bureaucratic obstacles.

Another example of reform, which had started under the Susilo Bambang Yudhoyono administration (with the 2009 Mining Law), was that the Indonesian government tried to reduce its dependency on exports of raw materials. With the 2000s commodities boom having ended it would make Indonesia much stronger if it could manage to process its mining and mineral output at home, and only thereafter export the processed products abroad. It was a painful process to force miners to establish smelting facilities and force foreign miners to divest shares so an Indonesian party (or several Indonesian parties) would control at least 51 percent of the mining company.

The 2009 Mining Law, which was designed with resource nationalism clearly in mind, essentially breached existing contracts with (foreign) miners as it disallowed exports of mineral ores (albeit the deadline was postponed) and forced foreign miners to become the minority shareholder (after 10 years of commercial operations). It certainly had a negative impact on the investment environment as it showed legal certainty is weak. However, lawmakers prioritized efforts to reduce Indonesia's vulnerable dependency on raw commodity exports.

This Section Is Being Updated