Cement Industry Indonesia

Cement is an important element for a nation's economy as this binder is a building material used for infrastructure and property development. As such, cement sales gives valuable information about savings and investment in a country. Rapidly accelerating domestic cement sales are a sign that the infrastructure as well as the property sectors are booming. The cement industry of Indonesia is a lively one. The country's total installed production capacity expanded from 37.8 million tons in 2010 to over 100 million tons in 2016, while domestic sales surged from 40 million tons to an estimated 60 million tons over the same period.

However, similar to other industries, Indonesia's cement sector has been plagued by Indonesia's economic slowdown that started in 2011. After rapidly rising cement sales in the years 2010-2012, sales started to slow from 2013 onward due to slowing economic growth, weakening purchasing power, low commodity prices, uncertainties surrounding the winners of Indonesia's 2014 legislative and presidential elections, and the higher benchmark interest rate (raised aggressively in 2013 in an effort to combat high inflation, the wide current account deficit and to support the ailing rupiah amid monetary tightening in the USA). Apart from the higher interest rate, Indonesia's central bank also implemented other measures that cooled the country's property market, such as a higher down payment requirement.

In 2016 this tighter monetary trend reversed. Bank Indonesia cut its key BI rate and raised the loan-to-value ratio for the purchase of a house in a bid to boost the nation's sluggish property sector. This may bring some new life in this sector in the second half of 2016. The residential property market accounts for the majority of cement demand in Indonesia and therefore the nation's cement players are eagerly waiting for a rebound in the property sector.

Read more: Overview & Analysis of Indonesia's Residential Property Sector

Despite the recent slowdown in Indonesia's property sector, the sector's long-term picture remains positive with the continuation of a rapidly expanding middle class. With rising per capita GDP people want to live in a better house. Moreover, Indonesia has a young population with about half of the population being below the age of 30 years. This implies that in the decade ahead there should be million and million of first-home buyers.

Cement consumption is still low in Indonesia with per capita cement production at approximately 300 kilogram. This figure is much lower than cement consumption in its peers Malaysia (over 600 kilogram per capita) or Vietnam. A low per capita cement consumption figure implies that infrastructure development is still underdeveloped in Southeast Asia's largest economy. The lack of quality and quantity of infrastructure is indeed one of the main bottlenecks in Indonesian society as it undermines connectivity thus seriously raising logistics costs, making businesses less competitive, while also causing social problems (for example because access to healthcare can be difficult in the rural regions).

Indonesian Cement Sales 2008-2016:

| Year | Cement Sales |

YoY Growth |

| 2016 | 62 million | +1.6% |

| 2015 | 61 million | +1.8% |

| 2014 | 60 million | +3.3% |

| 2013 | 58 million | +5.6% |

| 2012 | 55 million | +14.6% |

| 2011 | 48 million | +20.0% |

| 2010 | 40 million | +4.2% |

| 2009 | 38.4 million | +1.1% |

| 2008 | 38 million | - |

Source: Indonesian Cement Association (ASI)

Java, the most populous island of Indonesia, accounts for more than half of the country's total cement demand, followed by Sumatra.

Government-Led Infrastructure & Property Development in Indonesia

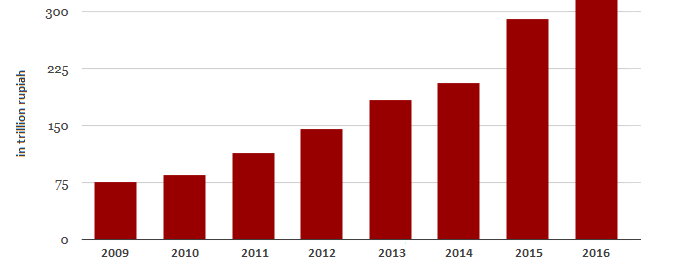

The Indonesian government, under the leadership of President Joko Widodo, has given more attention to infrastructure development in order to boost the country's economic growth in a productive way. The picture below shows that funds allocated to infrastructure spending has risen markedly in recent years (the steep rise between 2014 and 2015 was primarily caused by reallocating funds from energy subsidies - after scrapping costly gasoline subsidies in early January 2015 - to infrastructure spending). Obviously, sharply rising funds for infrastructure development across the archipelago will boost cement demand, provided that government spending goes smoothly. According to the latest reports, government spending on infrastructure development started to gain momentum in the second half of 2015 after a slow start in the preceding half.

In late-April 2015, the government also launched the "one million houses program", a government program that seeks to provide adequate housing facilities to low income citizens (more than half of these houses will be built using funds from the government’s state budget).

Another program that was launched in 2015 by Indonesian President Joko Widodo is the 35,000 MW power plant program through which the government aims to have added a total of 35,000 MW to the nation's existing power capacity by the year 2019. This implies that we should see the construction of many new power plants in the years ahead. Construction of a power plant requires cement.

Moreover, the new 2009 Mining Law of Indonesia, which includes a ban on exports of unprocessed minerals, encourages the development of domestic processing facilities (smelters). This ban came into effect in January 2014. However, due to the lack of domestic smelting capacity the government postponed the full ban until 2017 (some companies are allowed to continue raw commodity exports but have to adhere to strict regulations). Amid the low commodity price environment few miners are interested to invest in costly smelters and therefore we still expect to see robust smelter development in the years ahead, provided the Indonesian government remains committed to its latest policies. Just like power plants, the construction of smelters requires cement.

Funds Allocated to Infrastructure Spending in the Government's State Budget:

The three companies that dominate Indonesia's cement market are all publicly-listed on the Indonesia Stock Exchange. Indonesia's largest cement producer is state-controlled Semen Indonesia (formerly known as Semen Gresik). This company controls about 43 percent of the domestic sales market. The second-largest company is Indocement Tunggal Prakarsa with a market share slightly over 30 percent. On third place - with a market share of around 15 percent - comes Holcim Indonesia, part of the Swiss-based Holcim Group, one of the largest cement manufacturers worldwide. Smaller players include the Bosowa Corporation and Semen Baturaja. In recent years, a number of foreign cement companies (particularly from China) have entered the Indonesian market. The influx of new cement producers was reason why some government officials requested to implement limits to foreign investment in Indonesia's cement industry. The country's current cement production capacity already outpaces domestic cement demand and therefore the arrival of new players would only lead to a larger oversupply (particularly considering the big cement companies have plans to expand production capacity in the years ahead) hence causing lower selling prices and limited profitability.

Stock Performance Semen Indonesia (SMGR), Indocement (INTP) and Holcim Indonesia (SMCB):*

* normalized stocks, 1 January 2018 = 100

Cement companies in Indonesia were not amused when in early 2015 President Widodo ordered all state-controlled cement producers to lower selling prices of cement by IDR 3,000 per bag in order to boost growth in the infrastructure and property sectors. This also meant that non-listed cement producers had to follow suit in order remain competitive. However, this policy also reduced cement companies' profitability (and listed cement producers were hit by a sell-off in mid-January 2015).

In 2016 there arrived five newcomers in Indonesia's cement industry: (1) Anhui Conch (the local unit of China's cement giant Anhui Conch Cement Company) with its cement plant in South Kalimantan (having an annual production capacity of 1.55 million tons), (2) Pan Asia with its Semen Bima brand produced in the company's plant in Central Java (with an annual cement production capacity of 2 million tons), (3) Siam Cement - the unit of Thailand's largest cement producer - with its cement plant in Sukabumi (West Java) that has an annual installed production capacity of 1.9 million tons of cement, (4) Cemindo Gemilang with its plant in Banten (West Java) that has an annual production capacity of 4 million tons, and (5) Jui Shin Indonesia with its plant in Karawang (West Java) that has an annual production capacity of 2 million tons (its brand is called Semen Garuda).

The influx of new cement players - each providing additional cement production capacity to the nation's total capacity - implies that cement prices are under pressure. Several of the new cement companies offer their output at low prices in order to gain market share, despite domestic cement demand remaining relatively sluggish in the first quarter of 2016. The larger established cement companies of Indonesia may feel the need to join this price war in order to defend their market share.

Cement Export Indonesia

This also implies that Indonesia's cement companies should focus more on the export of cement, which is currently insignificant. Indonesia's cement exports declined heavily between 2007 and 2012 due to rising domestic cement demand (particularly caused by the country's property boom). However, as cement production capacity has expanded rapidly in recent years - exceeding domestic demand - there is again room to focus on export markets. Several interesting export markets for Indonesian cement include Bangladesh, Africa, Australia, the Philippines and the Middle East. In recent years exports of Indonesia's largest cement producers has increased.

Cement Exports of Indonesia's Top 3 Cement Producers:

| Company | 2014 |

2015 |

| Semen Indonesia | 1,376,174 | 1,388,459 |

| Indocement Tunggal Prakarsa | 156,504 | 212,500 |

| Holcim Indonesia | 77,722 | 227,524 |

in IDR million

Various sources

Updated on 30 May 2016